Which Neighborhoods Have Appreciated Most and Why?

4th Quarter 2014, Paragon Special Report

———————————————————————

Percentage Appreciation Rates

2010/2011 – Present

This analysis is based upon review of both median sales price and average dollar-per-square-foot data. However, there is no San Francisco or Noe Valley median or average home that one can use as the unchanging basis for comparison year after year, only differing collections of unique homes selling in different times and circumstances. Please see notes at the end of this report regarding our methodology.

Adjusting your screen-view to zoom 125% or 150% will make the charts easier to read. A San Francisco neighborhood MAP can be found at the bottom of this webpage.

The above chart illustrates the approximate home value appreciation from the bottom of the market (2010-2011) to present (2014 YTD), as illustrated by the dark gray bars, and the overall appreciation or depreciation to date since the last market peak (2006-2008), as illustrated by the red numbers.

Over the past 3 years, in our latest market recovery, San Francisco neighborhoods have typically appreciated 40 – 50%, with an overall increase of approximately 44%. This correlates well with the Case-Shiller Index for the Metro Area, which estimates appreciation in the range of 42% – 46% for Bay Area mid and high-priced homes. As one can see in the percentages in red, most of the city’s neighborhoods have now exceeded, often by substantial margins, their previous peak values before the bubble popped. However, some of the neighborhoods hit hardest by the subprime crisis are still below their previous peaks.

Looking at the 3 neighborhoods with the highest appreciation rates from the bottom of the market to present, there are distinctly different reasons why they stand out:

- Bayview: Up 75% from 2010/11; but still down 12% from its market peak in 2006. Due to subprime lending, Bayview’s bubble was so big, its market crashed terribly when it popped. During the downturn, its housing market became dominated by distressed sales and it fell so far that now, with the disappearance of the subprime effect, its recovery has been equally dramatic. But because its bubble was so large, it is still below its 2006 peak value. The markets in the Bayview and nearby neighborhoods are quite strong, because they contain the most affordable houses in the city.

- Inner Mission: Up 63% from 2010/11; up 46% from 2007 (pre-crash peak). The Mission’s appreciation rate is explained by a huge change in its buyer demographics over recent years: Though it had been slowly gentrifying since the nineties, more recently it became a highly sought-after home location for young, hip, affluent, high-tech buyers. They love the Valencia Street corridor, being close to Dolores Park, the sunny weather and the (disappearing) edginess – and the speed of gentrification shifted into a feverishly high gear. This change has also entailed the construction of expensive, new, condo projects (typically selling for $1000 per square foot and up), which is also pushing up average and median values.

- Bernal Heights: Up 57% since market bottom; up 24% from its previous market peak in 2007. Bernal Heights has become one of the most popular, more affordable, go-to neighborhoods for house buyers who like the neighborhood ambiance of the general Noe Valley area, but were priced out there by its rocketing prices. Bernal Heights’ houses – with a median price about 45% lower than Noe Valley’s – have looked likeextremely good values in comparison. Buyer competition for new listings became particularly fierce in the past year or so.

———————————————————————

To give context to the appreciation rates, this next chart delineates actual 2014 YTD median home sales prices. In the second half of 2014, after a frenzied spring market, appreciation generally flattened or even ticked down a little in the more expensive areas of the city, but continued to tick up in the more affordable districts. On the other hand, the more expensive neighborhoods began their recoveries in late 2011 and early 2012, much earlier than the less affluent districts.

———————————————————————Dollar Appreciation Rates

Whether you are a buyer, seller or real estate agent, dollars are more real than percentages: Hearing that a home has jumped hundreds of thousands of dollars in value in a relatively short time period grabs the attention more than a percentage change. The higher priced neighborhoods sometimes have lower percentage appreciation rates than less expensive areas in a given time period, but the dollar-amount changes can make the eyes pop:

In Pacific & Presidio Heights, the theoretical “median house” now costs over $1.3 million more than it did 3 years ago. In Noe, Eureka & Cole Valleys, the increase is over $700,000.

———————————————————————Boom, Bust, Recovery

2000 – 2014

Different neighborhoods and price segments experienced bubbles, crashes and now recoveries of significantly different magnitudes. The city’s less affluent neighborhoods – on this chart illustrated by Bayview, Excelsior & Portola – had much bigger bubbles and subsequently much bigger crashes, both inflated by subprime lending issues. Bayview saw an astounding 136% appreciation from 2000 to 2006, followed by a huge 50% drop from 2006 to 2010/2011. Excelsior and Portola were an order of magnitude behind with 90% appreciation and 30% decline. Generally speaking, the mid and high-end segments of the city’s market appreciated 60% – 70% from 2000 to pre-crash peak, and then dropped by 15% to 20% subsequent to the 2008 market crash. And, as mentioned earlier, on average the city’s home values have now increased 40% – 50% over the past 3 years, with some neighborhoods outperforming the general range.

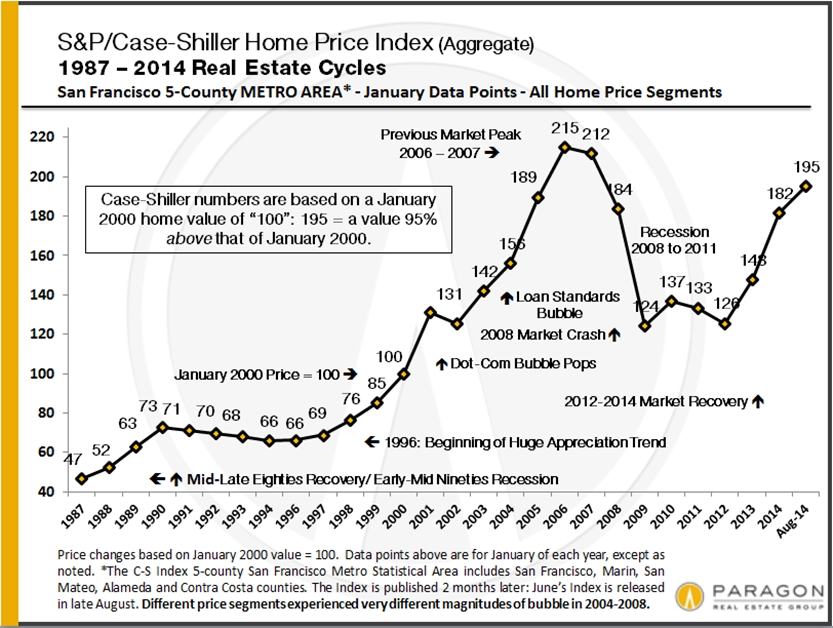

According to the Case-Shiller Home Price Index, Bay Area homes of all price segments are now, regardless of their different ups and downs over the past 15 year, about 96% above their prices in year 2000 (as of late 2014). This may suggest that an equilibrium is being achieved in the market.

Note that the tremendous burst in home price appreciation actually began in 1996, subsequent to the early nineties recession. Prices approximately doubled in the 5 years 1996 to 2000. This earlier period is not included in these charts, nor is the smaller, short-term decline following the dotcom bubble bursting in 2001 broken out.

———————————————————————Housing Cost: Today vs. Previous Peak Values

Comparing current San Francisco home values to previous peak values before the 2008 financial markets crash, we estimate general home-price appreciation in San Francisco of approximately 15% to 20% over the past 7 years. However, mortgage interest rates are now about 35% lower than in 2007 and there has been inflation of approximately 15% over the same period. Thus, we estimate that, adjusting a normal 20% – 25% down-payment plus resulting loan expense to 2007 dollars, the current cost of housing – mortgage and property taxes – is about 12% lower now than it was in 2007. This is a back-of-the-envelope calculation based on a number of basic assumptions – and it would obviously vary widely by neighborhood – but we believe it to be generally valid.

The Bay Area’s current market recovery has lasted about 3 years now. Over the past 35 years of cycles, recoveries have typically lasted in the range of 5 to 7 years, which doesn’t guarantee that this one shall follow past patterns.

———————————————————————

Important notes regarding this report:

The estimates in this analysis should be considered very approximate since there are different ways to evaluate home value movements – such as median price and average dollar per square foot – and they don’t always agree, nor are they perfectly reliable. Besides which, other factors can affect these statistics besides changes in values, such as big changes in the distressed, new-construction or luxury home segments. There are also a wide variety of economic and political factors that can and do impact real estate markets.

Different San Francisco neighborhoods peaked in value at varying times before the bubble popped on 9/15/08: Generally speaking, the least affluent areas peaked in 2006; the mid-price segment in 2007; and the high-end market hit peak prices in late 2007/early 2008. We use the 2-year period of 2010-2011 as the basis for “bottom of the market” values, and we use aggregate 2014 YTD values (as of mid-late November) for “present” values. If one cherry-picked specific months or quarters for the absolute lowest and highest values in each neighborhood, the percentage and dollar swings illustrated would be much more dramatic than with the broader periods used in this report, but, we believe, no more meaningful.

This map of neighborhoods is according to the San Francisco Association of Realtors,

SAN FRANCISCO REALTOR DISTRICTS

District 1 (Northwest): Sea Cliff, Lake Street, Richmond (Inner, Central, Outer), Jordan Park/Laurel Heights, Lone Mountain

District 2 (West): Sunset & Parkside (Inner, Central, Outer), Golden Gate Heights

District 3 (Southwest): Lake Shore, Lakeside, Merced Manor, Merced Heights, Ingleside, Ingleside Heights, Oceanview

District 4 (Central SW): St. Francis Wood, Forest Hill, West Portal, Forest Knolls, Diamond Heights, Midtown Terrace, Miraloma Park, Sunnyside, Balboa Terrace, Ingleside Terrace, Mt. Davidson Manor, Sherwood Forest, Monterey Heights, Westwood Highlands

District 5 (Central): Noe Valley, Eureka Valley/Dolores Heights (Castro, Liberty Hill), Cole Valley, Glen Park, Corona Heights, Clarendon Heights, Ashbury Heights, Buena Vista Park, Haight Ashbury, Duboce Triangle, Twin Peaks, Mission Dolores, Parnassus Heights

District 6 (Central North): Hayes Valley, North of Panhandle (NOPA), Alamo Square, Western Addition, Anza Vista, Lower Pacific Heights

District 7 (North): Pacific Heights, Presidio Heights, Cow Hollow, Marina

District 8 (Northeast): Russian Hill, Nob Hill, Telegraph Hill, North Beach, Financial District, North Waterfront, Downtown, Van Ness/ Civic Center, Tenderloin

District 9 (East): SoMa, South Beach, Mission Bay, Potrero Hill, Dogpatch, Bernal Heights, Inner Mission, Yerba Buena

District 10 (Southeast): Bayview, Bayview Heights, Excelsior, Portola, Visitacion Valley, Silver Terrace, Mission Terrace, Crocker Amazon, Outer Mission

Some Realtor districts contain neighborhoods that are relatively homogeneous in general home values, such as districts 5 and 7, and others contain neighborhoods of wildly different values, such as district 8 which includes both Russian Hill and the Tenderloin.

———————————————————————Statistics are generalities that may fluctuate for a number of reasons, including but not limited to changes in home values. There is no San Francisco “median home” or “average home,” that one can use as the unchanging basis for analysis year after year, only differing collections of unique homes – and how these general statistics apply to any particular property is impossible to say without a custom market analysis. These analyses were performed in good faith with data derived from sources deemed reliable, but they may contain errors and are subject to revision. All numbers should be considered approximate.