George may have left office a year ago, but there appears to be a growing consensus that the likely shape of the recovery will be a “W.” How appropriate, if you believe that we are reaping the bitter fruit of his administration’s policies.

A front page article in the Business Section of last Wednesday’s New York Times, grimly entitled “An Upturn in Housing May be Reversing,” pulls together recent and contradictory data from various sources, including Case-Shiller, Moody’s, and The National Association of Realtors. The conclusions are sobering.

There is a growing consensus that the positive national sales data that we’ve seen over the last few months is faltering. Much of the recent activity, for example, was stimulated by the anticipated expiration of the “First Time Home-buyer Tax Credit,” originally set to expire in November, and now extended through April of next year. Essentially, this means we’ve “borrowed” from future sales.

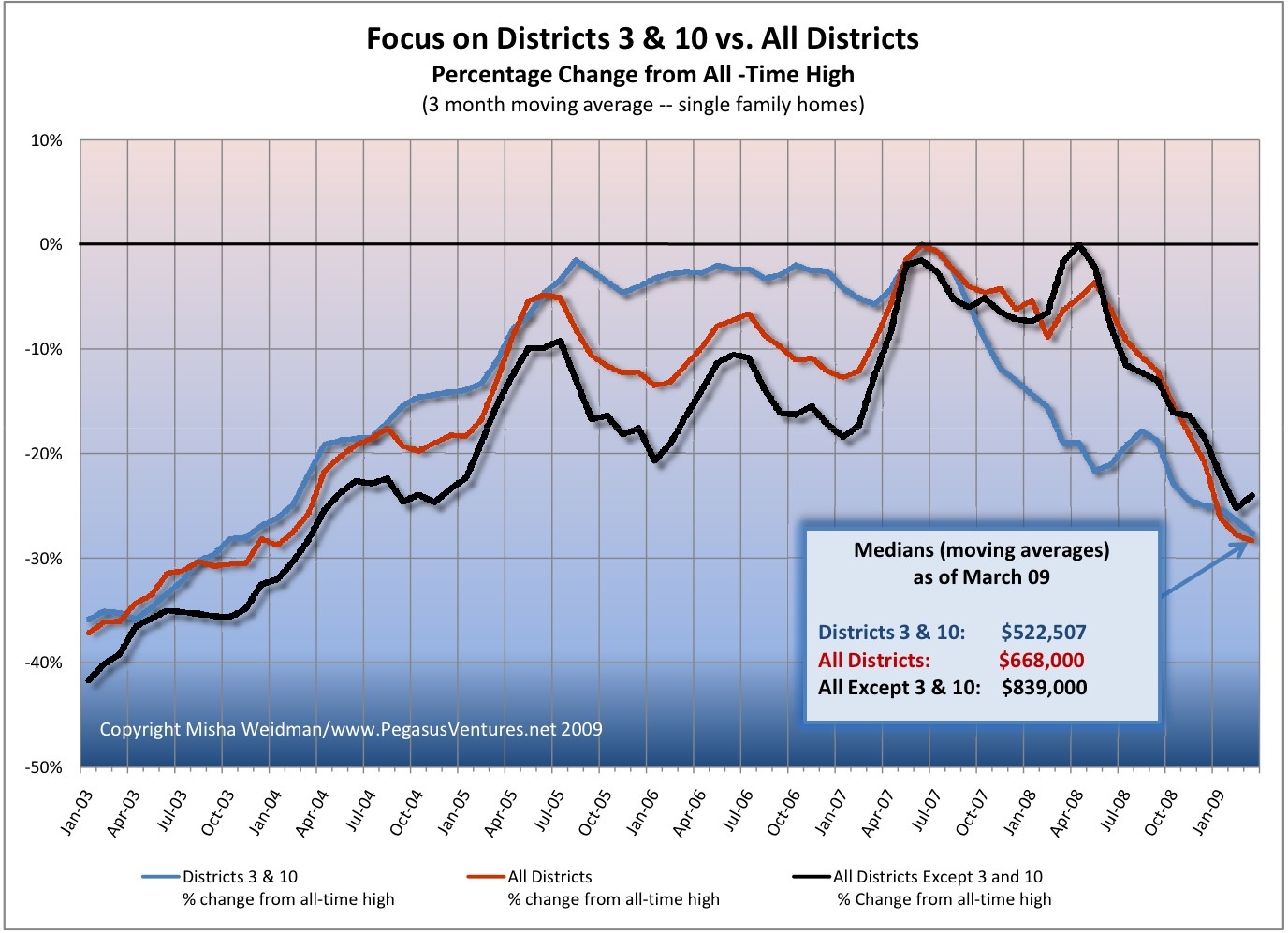

Also, despite some positive economic news and decent sales volumes, there’s been little improvement in sales prices because inventory levels – read “foreclosed properties” – remain so high. Mary Maitland, VP of the S & P Index that publishes the Case-Shiller Index foresees a “W” pattern for the housing market, with prices this winter testing the lows we saw earlier in the spring. Am I allowed to say “I told you so?”

The NY Times article has a cool interactive chart for specific MSA areas including “San Francisco” — remember this covers 5 of the 9 Bay Area Counties.

Where do you think the market went in 2011? Come on. Take a guess. If you believe my own SF Association of Realtors “stronger affordability conditions, a lower cost of owning versus renting, and declining foreclosures, continue to steer the San Francisco housing market in a positive direction.” [January 2012 Market Focus Report].

Where do you think the market went in 2011? Come on. Take a guess. If you believe my own SF Association of Realtors “stronger affordability conditions, a lower cost of owning versus renting, and declining foreclosures, continue to steer the San Francisco housing market in a positive direction.” [January 2012 Market Focus Report].