Back in February I posted about two $2.1 million homes offered for sale in my ‘hood. 731 Douglass had 3,000 square feet of good, livable space and the sorts of finishes and flourishes you’d expect. But it had no back yard and was located on the fairly busy corner of 24th Street and Douglass, with a Muni stop and Noe Valley Courts’ sand-pit within spitting distance of the front windows.

Meanwhile 110 Hoffman, offered at just $2,000 less than Douglass, had a little less space and a vertical, less user-friendly lay-out. But, location it had in spades, on one of Noe’s best and quietest streets. Plus it had a spacious back yard with a lovely mature tree.

My good friend and blogging critic, Mike Dashe — the American part of the Franco-American wine-making duo who own Dashe Cellars — recently took me to task for not doing what any good story-teller does: tell ’em how it ends. So here’s the final chapter folks.

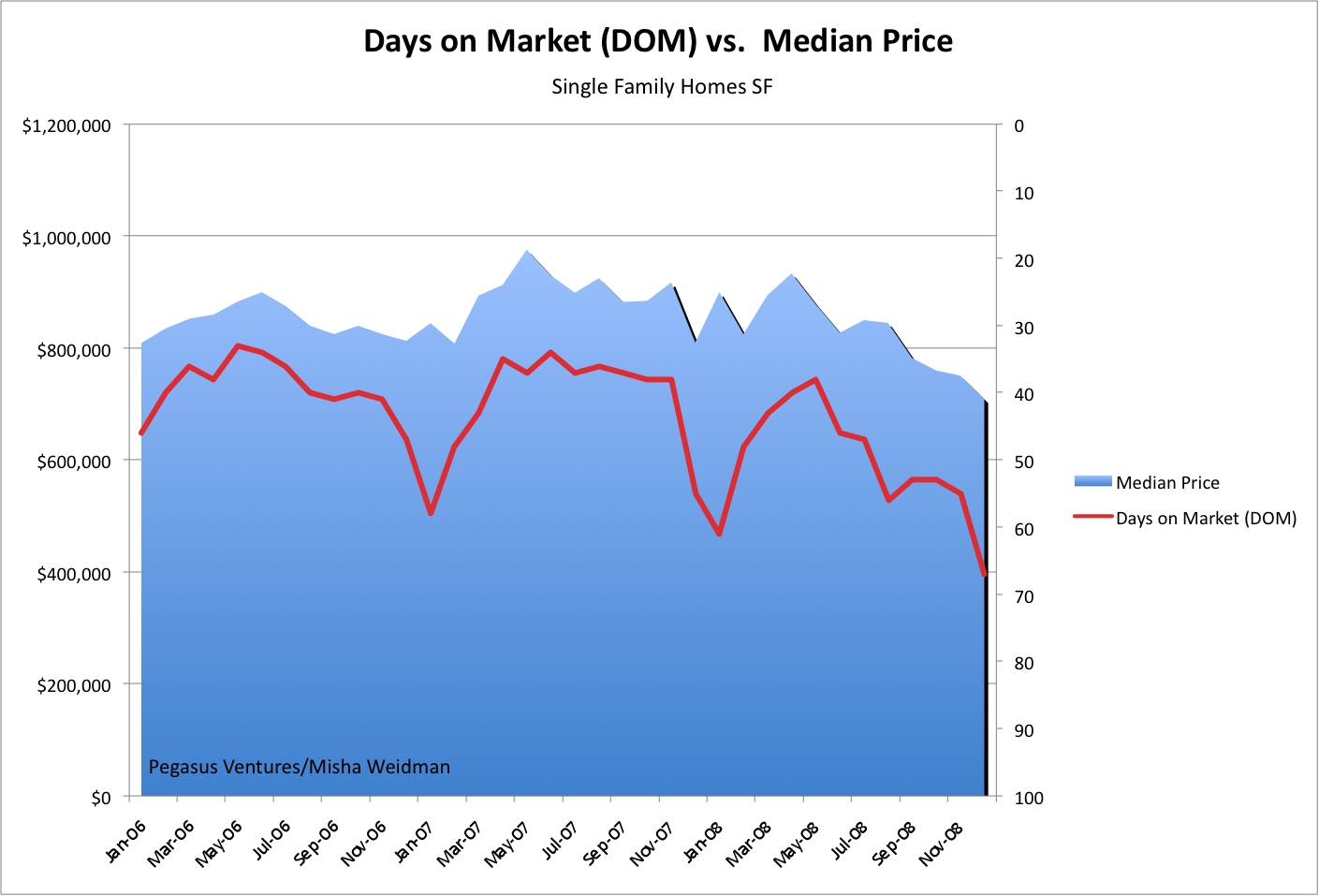

731 Douglass came in first, selling for a respectable $1.85 million, or 85% of the listing price after just 48 days. Good show! Though it’s worth noting that this was a cool $100,000 LESS than it sold for back in March 2005, when it was on the market for just 18 days. (There’s more proof of the correlation between price and DOM — days on market — see my previous post.)

110 Hoffman had a more torturous ride to the finish-line. Originally listed at $2.395 million, it suffered two price drops and was ultimately withdrawn from the market 102 days later when it failed to sell at $2.148. Fast-forward five months to July and it’s back on the market at $1.995. And, after falling in and out of contract, and back in — it sells for….

$1,995,000. Full list price and all within 10 days if the MLS Database can be believed.

That’s a cool $100k more than 731 Douglass.

What went on here? I honestly don’t think this was a case of location trumping space. Instead, it’s about timing. 731 Douglass went on the market in January and sold in March. Prices generally fall somewhat during winter months. But much more importantly, does anyone remember how the financial world was coming to an end right at that time? The stock market was dropping like a stone and no one knew where it would end. (In fact, the S&P 500 hit bottom on March 9.)

I remember when I had the misfortune of putting the first property I ever owned on the market not long after 9/11/01. I’m convinced that it sold for around $300k less than it would have at any other time.

Seen in this light, it sure seems like the owners (and the agent) of 110 Hoffman made the right decision to bide their time. A few months later, the sun breaks out literally and metaphorically and things are moving again. Here’s a case where the tortoise beat the hare.

And speaking of odd-looking creatures, let’s get back to Dashe Cellars and their beautiful wines (you gotta try their single vineyard Zins.) Mike, would you care to explain what’s with the monkey and the, ahem, “whale?”