While single family home prices for San Francisco as a whole can’t seem to recover beyond being around 18% down from their all-time highs, Noe Valley home prices have come roaring back since the start of the year. The three month moving average for April was down just 1% from its all-time high of March 2008. In May, the moving average slipped back to 6.5% off the all-time high. Take a look (click to enlarge): Continue reading “Noe Valley Comes Roaring Back”

How Deep is Noe’s Valley?

Judging by the number of houses I’ve seen being redone from the studs up, together with the number of homes that seem to be hitting the market at over $2 million these days, you’d think that Noe Valley real estate is doing very well once again, thank you very much.

Exhibit A: 729 Elizabeth Street. Continue reading “How Deep is Noe’s Valley?”

Double Dip — Again?

Woke up this morning to NPR announcing that new home sales were the lowest they’d been in 15 years. The housing market is already in a double dip, with some additional price declines on the horizon, though we’re near the bottom. As for the broader economy, we’re skating awfully close, but nobody really knows yet whether we’ll eke out some anemic growth or slide back into recession.

This charming news was followed by another bit of analysis that makes so much sense in retrospect that I’m surprised we haven’t heard it stated more often. What’s well known is how the wave of foreclosures has affected millions of people directly and the corresponding effect on the economy as they lose their homes, their savings, and their credit ratings. But second only to that in terms of its drag on the economy is the effect that declining values have had on people’s ability to move to where the jobs might be. Simply put, there’s a huge number of people who would move, but they can’t because they’re so underwater on their homes. Since they can’t move, they remain unemployed or underemployed, and since there won’t be any significant recovery in the housing market until jobs come back, they remain stuck in a vicious downward cycle. You can find the transcript here.

And a post script. You may have noticed a drop-off in my blogs lately. Summer vacation and the need to work on my development project have taken a toll on the amount of time I have had available to research and write. But don’t erase me from your blog roll yet, please! My eyes and ears are open, and I will try, try, try to post more often as soon as I get my head above water.

Related articles by Zemanta

- For Most People, The Double-Dip Has Arrived (businessinsider.com)

- Moody’s Zandi Predicts 1 in 3 Chance of a Double-Dip Recession (wallstreetpit.com)

- Rate-Setter: ‘Foolish’ To Rule Out Double Dip (news.sky.com)

Continued Improvement in the Housing Market or Borrowing from the Future?

The National Association of Realtors (NAR) reported yesterday that existing home sales in October rose to their highest level in more than two years. Nationally, sales were up 10.1% over September and up 23.5% year over year.

Most of the increase in sales, however, was not in the western region, where sales were only up 1.6% from the previous month. (Oh, the devil is always in the details.) And more “good news”: The western region median price of $220,200 — clearly this is not San Francisco — was down 14.7% year over year.

Not surprisingly, the article stresses the positive. Inventories are shrinking, especially at the lower price levels where foreclosures and REOs are slowly being digested by the system. Prices have fallen by the smallest amount in over a year (don’t you love that!).

You can argue that any press release by NAR is going to be self-serving, but its Chief Economist, Lawrence Yun, doesn’t mince words when he says that a lot of the sales surge was fueled by the anticipated expiration of the First Time Homebuyer Tax Credit. The $8,000 tax credit was originally scheduled to expire in November, but has now been extended through April 30, 2010. Yun goes on to caution that “with such a sale spike, a measurable decline should be anticipated in December and early next year before another surge in spring and early summer.”

We can only hope that he’s right about that surge….

Dead Cat Bounce?

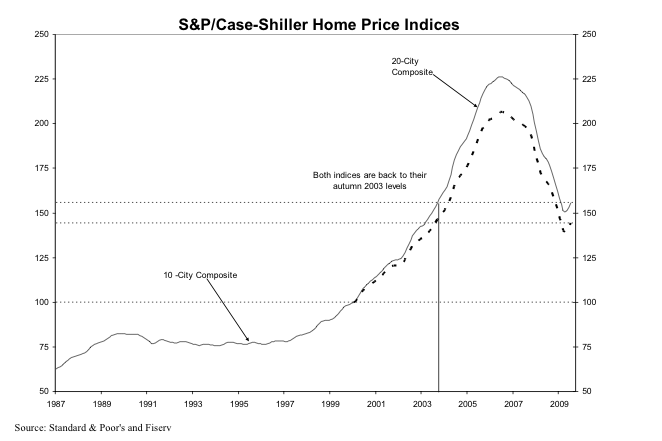

At the end of last month, the media was full of Case-Shiller’s upbeat report on the national housing market for July 2009, its most recent reporting month. Three months of improving sales “continue to support an indication of stabilization in national real estate values,” according to the September Report.

Here’s the chart, by the way, which also shows that on a national basis we are back to Autumn 2003 price levels.

See that little up-tick at the very end of down side of the mountain? That’s what every one is celebrating, folks. Indeed, it’s hard not to laugh when the Report includes tortured phrases like “the rate of annual decline … seems to be decelerating” or “all metro areas are showing an improvement in the annual rates of return, as seen through a moderation in their annual declines.” Whoopee!

Locally, “San Francisco” — keep in mind that for the CS Index, this means 5 of the 9 Bay Area Counties — posted its fifth straight gain, with a seasonally adjusted gain of 2.9% over June 09, which followed a seasonally adjusted gain of 3.2% in June over May. Before you break out the champagne, “San Francisco” was still down 17.9% year over year.

This is now old news. But in this Sunday’s New York Times, Mr. Shiller mused about what all this meant for the real estate market. The article is not a model of clarity, but Shiller’s conclusion is pretty stark: “At the moment, it appears that the extreme ups and downs of the housing market have turned many Americans into housing speculators.” He suggests that people are looking at the huge amount of money the fed is pumping into the system, the first-time home-buyer tax credits, and other short-term infusions, and basically “trying to time their home-buying decisions” and thus artificially causing the spike in prices. Here’s the takeaway: “The sudden turn could signal a new housing boom, but it is more likely just a sign of a period of higher short-run price volatility.”

Indeed, after noting that the recent change in direction in the CS Index is the sharpest he’s ever seen, he takes a look at the last time a similar turnaround occurred. It was at the end of the last housing bust, after the 1990-91 recession. Five years later, however, home prices were down 13.8% in inflation-adjusted terms from the highs they’d reached in the “turnaround” month.

Meanwhile, the stock market continues its giddy gains — perhaps for many of the same reasons as the housing market has bounced back.

Personally, I’m not terribly fond of cats, but if I owned one I’d be keeping it away from any open windows.

Homes vs. Condominiums: How much extra do you pay?

Recently, I blogged about the fact that condominiums seemed to be holding up better than single family homes in terms of their decline from their all-time highs.

At the same time, I noted that there was only about $100,000 difference in median value between condos and homes. That seemed like a small delta and I was interested to see whether it was, historically speaking. Turns out that it is.

Since, until recently (ahem!), home prices along with everything else have tended to go up, I decided not to look simply at the difference in price between condos and homes. Instead, I converted the price difference to a percentage of the median value of condos sales for the given period. This represents the “premium” for owning a home rather than a condo. Here’s the result.

Sure enough, you’d normally expect to pay around 20% more for a home than for a condo. But starting in 2008, the home “premium” started dropping significantly. I believe that drop was a direct reflection of the housing market decline that began with homes and only subsequently spread to condos. As I postulated in my blog, condo values possibly held up for longer as people got squeezed out of the single family home market by tightening credit standards.

But what about 2009? The chart above shows the premium based on all sales for the year to date. The picture looks a little different if you look at values on a monthly basis.

Again this is consistent with my previous blog. It suggests while that condo values may have held up longer, they too have fallen so that the premium paid for a home is now heading back to its historic norm. Of course, the other possibility is that home prices are beginning to recover. It may well be that both explanations are true.

More Grim News on Housing

Saturday’s NY Times proclaims “A Gloomy Outlook for Home Sales’ Big Season.” The headliner, by the way, was “Job Losses Hint at Vast Remaking of U.S. Economy.” Is it really any wonder we have difficulty sleeping a’ nights?

{kind=link}

Here are some of the cheery highlights:

- One out of every seven apartments and houses in the US are vacant, a level not seen since the 1960’s. That’s about 19 million units

- Less than a third of those are actually for rent or for sale, meaning that many more could yet come onto the market.

- New contracts for previously owned homes fell at their fastest pace for two years.

- Some areas that have fallen fastest, like inland California, are seeing improved sales.

- Urban areas that have withstood the recession reasonably well, like San Francisco and New York, are “frozen.”

We pass Elk Grove on our way up to Tahoe. Beautiful spot east of Sacramento. You can buy a 3 BR house there for $193,000. The same house sold for $336,000 four years ago. The mortgage is a $100 less than it costs to rent a 2BR apartment. It’s hard not to think of that as positive. That is, unless you were the one who lost $143,000 in equity.

They’re predicting the housing market will get “worse” before it gets better. Why “worse”? Because a lot of people are going to feel — and be — a hell of a lot poorer than they used to. And the people for whom an increase in housing affordability might make a difference are the ones who are getting hammered the worst.

Here’s a chart showing future’s contracts on home prices. It shows prices deteriorating further this year, followed by a long, flat recovery starting some time in 2010.

Sounds like it’s going to be chilly spring.