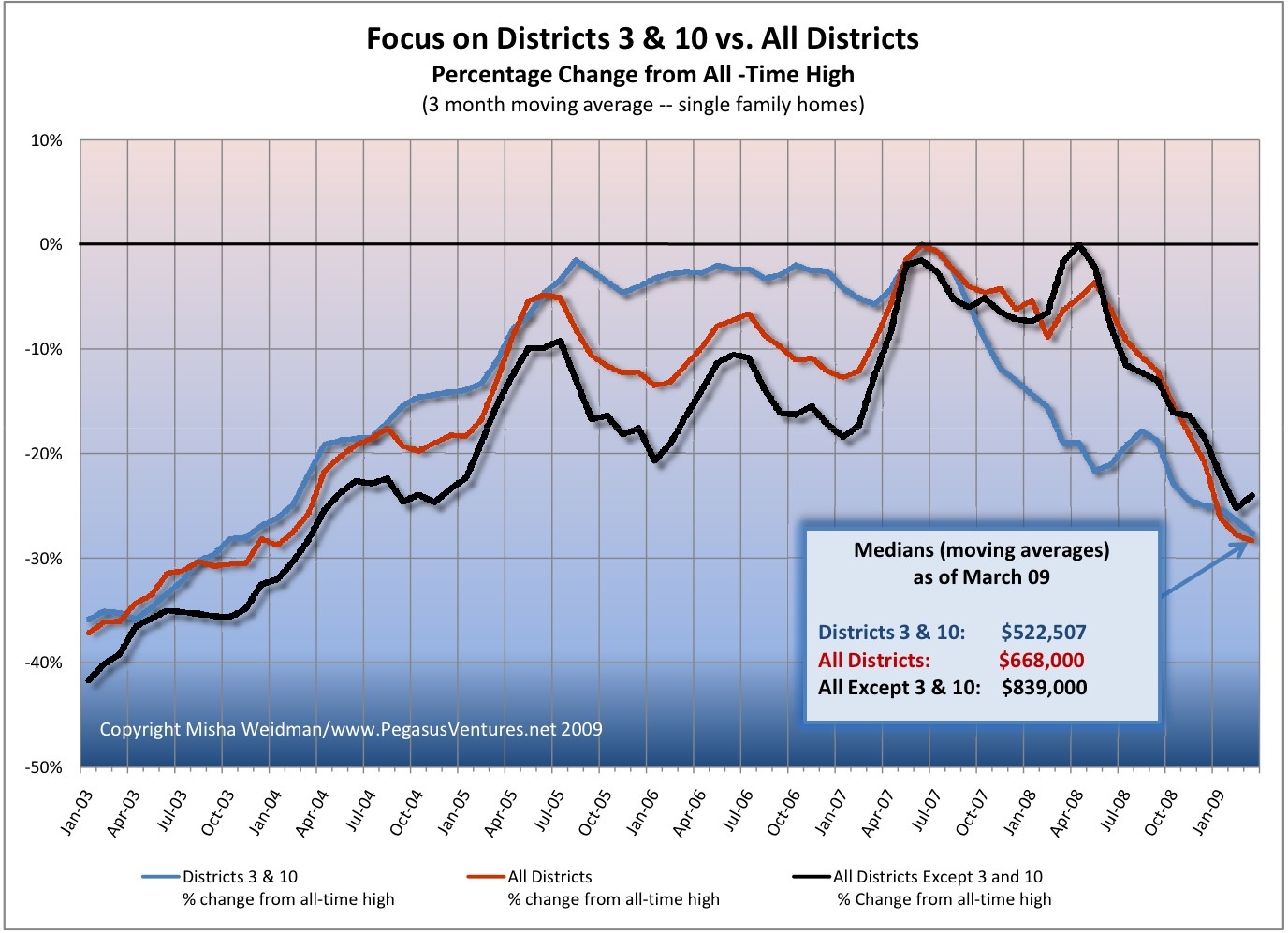

For the quarter century (gulp!) that I’ve been involved in real estate, the conventional wisdom has always been that condo values generally do worse in down markets than homes. Why? To be honest, I’m not sure, but I think it’s because it’s easier to overbuild the condo market than the single family home market. It goes back to that famous quote: “Buy land – they aren’t making any more of it.” Just take a look at Miami, Chicago – or downtown San Francisco. One new high-rise can hold hundreds of condos in the sky. Try building just one new home in SF, let alone hundreds – it aint happening.Of course, more supply + less demand in a down market means prices fall. Has that been the case in San Francisco?

I looked at percentage change from all time highs for condos and single family homes (sfd’s) since January 2003 and here are the results for the city as a whole.

Until June 2008, condo and home prices were in lock-step in terms of price appreciation and decline. Thereafter, homes fell first and further. (Do I hear a lithp?) In March 2009, the delta between condos and home prices was a whopping 13%. Since then, however, home prices have recovered smartly: as of June, homes are about 4.5% further off their all-time highs than condos.

What does this all mean? First of all, I wouldn’t take too much consolation just yet in the upward spike in both condo and home prices since the beginning of the year. If you take a look at the chart, this happens every Jan/Feb when people start buying out of the winter doldrums. I wouldn’t predict a bottom until we see what happens this winter.

Secondly, given the woeful condition of the economy and the credit markets, together with the fact that San Francisco is not a badly overbuilt housing market, it sort of makes sense that condos are holding their value relatively well as people are finding themselves priced out of more expensive single family homes.

Still, the current delta of only $100,000 between median condo and median home prices seems rather small. If people are just begging to know what the historical average is, let me know and I’ll find out.