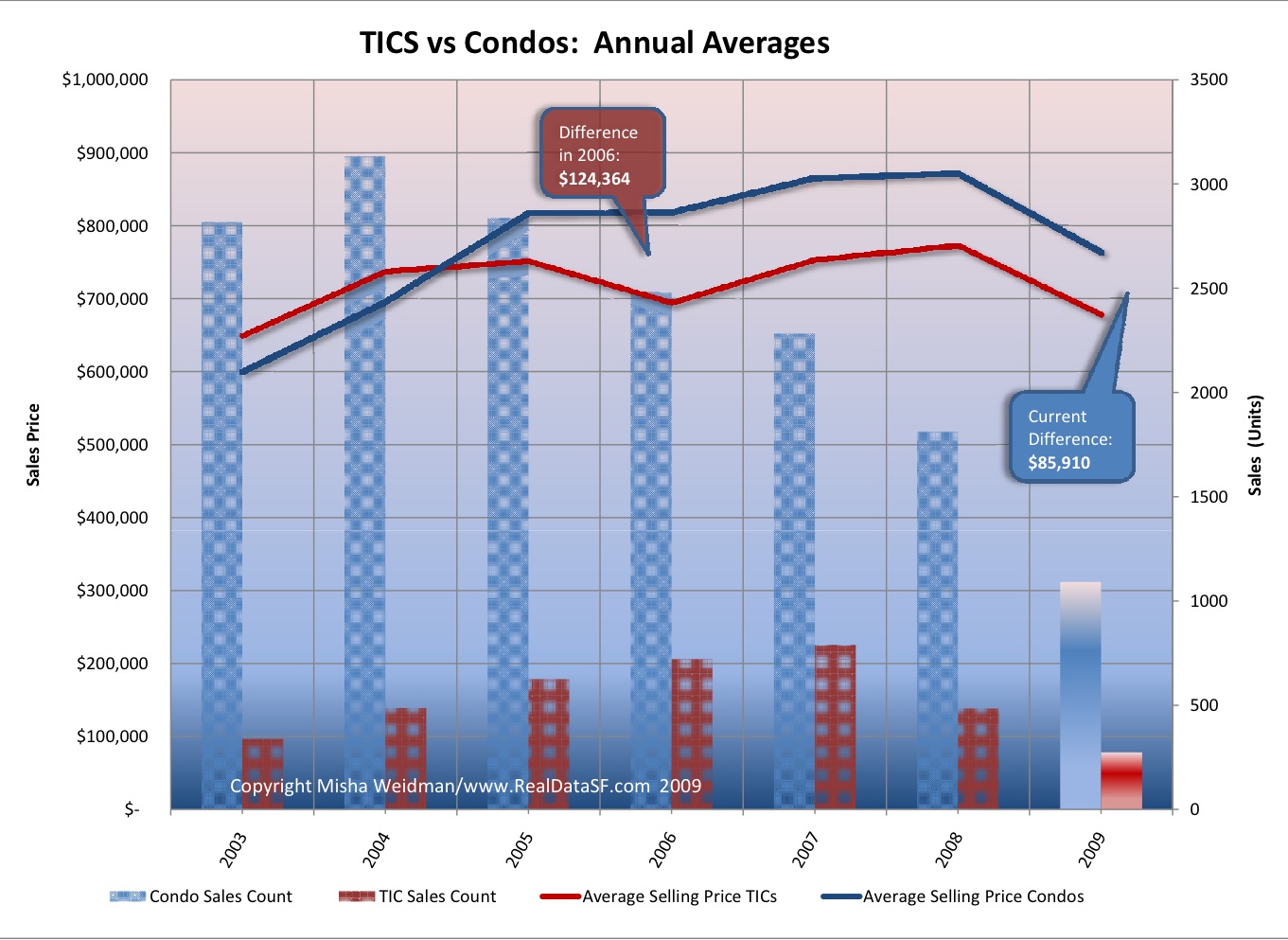

Last post, we determined that the current difference between the average (annual) price of a condo and that of a TIC is $86,000, down from a high of $124,364 in 2006. (That’s a 30%+ drop, by the way.) Here’s the chart again (sorry for the funky transparency on the sales volume bars).

That’s useful if you’re looking at an average-priced TIC and you’re curious about how much of a premium you’d have to pay for an average-priced condo. But how about reducing that to a per square foot premium?

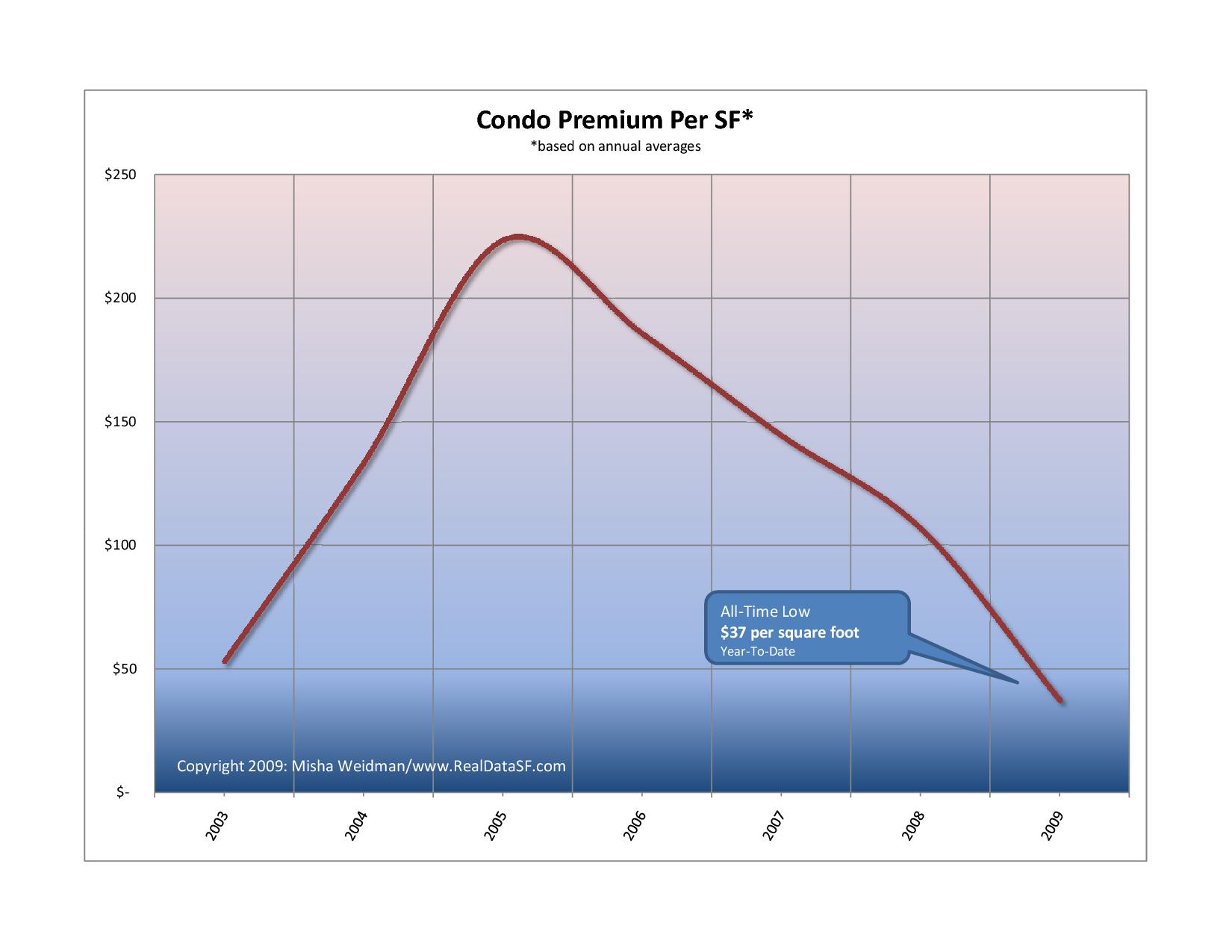

For those who just want the bottom line, here’s the answer, but it’s worth reading on for the caveats.

$37 a foot doesn’t sound like much of a condo premium to me, that’s for sure. And as my astute readers will note, the drop in price on a per square foot (from around $225 per sf) is obviously much more than the drop in median sales prices shown in the previous chart.

What’s going on? It’s really simple: there’s a lot less information on sales price per square foot for TICs.

All my data comes from the MLS (Multiple Listing Service) that real estate brokers use to find and market properties. When a sale’s completed, they are required to enter the sales price. If there’s information on the square footage of the property — provided by the owner or more frequently from the property records — the database calculates a per square foot price. Roughly 80% of condo sales have a recorded price per square foot in the MLS. Only 45% of TIC sales have a recorded price per square foot. How bad is that? In September 09, there were just 27 TIC sales. Only 9 of them had a recorded price per square foot. For all of 2009 through September, there were 275 TIC sales. Only 113 – 41% – show a per square foot price.

There are lots of people — mostly on other blogs 🙂 — who love to trash statistics and say they’re meaningless. Medians don’t reflect home values, etc etc. I disagree. Provided you have enough data and you understand what you’re measuring, statistics help make sense out of what is otherwise undifferentiated data. But I am afraid that in the case of measuring the condo premium on a per square foot basis, we are in dangerous low on data.

One final reminder: For this series of posts, my TIC data includes the handful of stock cooperative sales that occur in this market.

And thanks for sticking with me on this long series of posts….