I remember how the world changed on September 11, 2001. There was the horror of the actual event, the new sense of our own and our loved ones’ vulnerability to a random death. There were the new protocols for entering public spaces and traveling, the scanning of faces and backpacks that we’d never done before. And there was grief. We mourned not just the catastrophe but an irredeemable loss of innocence – not mankind’s first, and certainly not its last, but no less wrenching for that.

The current crisis feels both similar and different. Unlike 9/11, the streets remain eerily empty. Restaurants and cafes are still shuttered. We aren’t flocking together for comfort – we’re staying apart, isolated. What’s similar is the pervasive sense that the worst is yet to come; that there’s a tsunami forming and very little we can do to avoid it crashing down us; that we are all much more mortal than we thought we were three weeks ago.

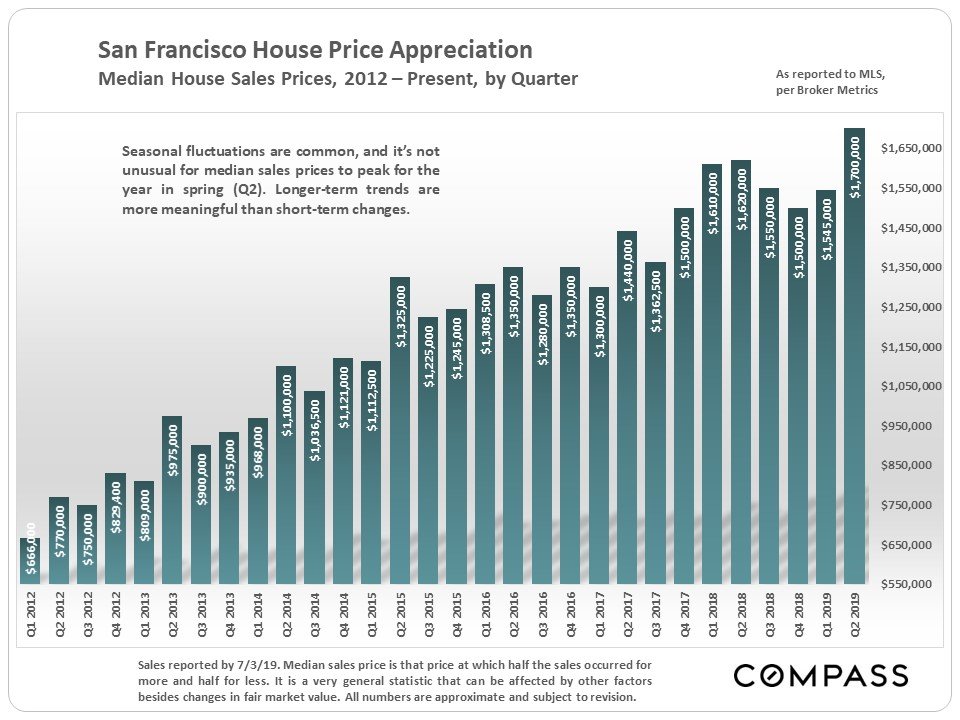

And now, as then, we go on. We adapt. We make the best of things and plan for the future. In that spirit, I offer some insights on what Covid-19 is doing to San Francisco’s residential market.

The following chart tracks the number of new listings on the Multiple Listing Service (MLS) by week. It might just as well track human sentiment.

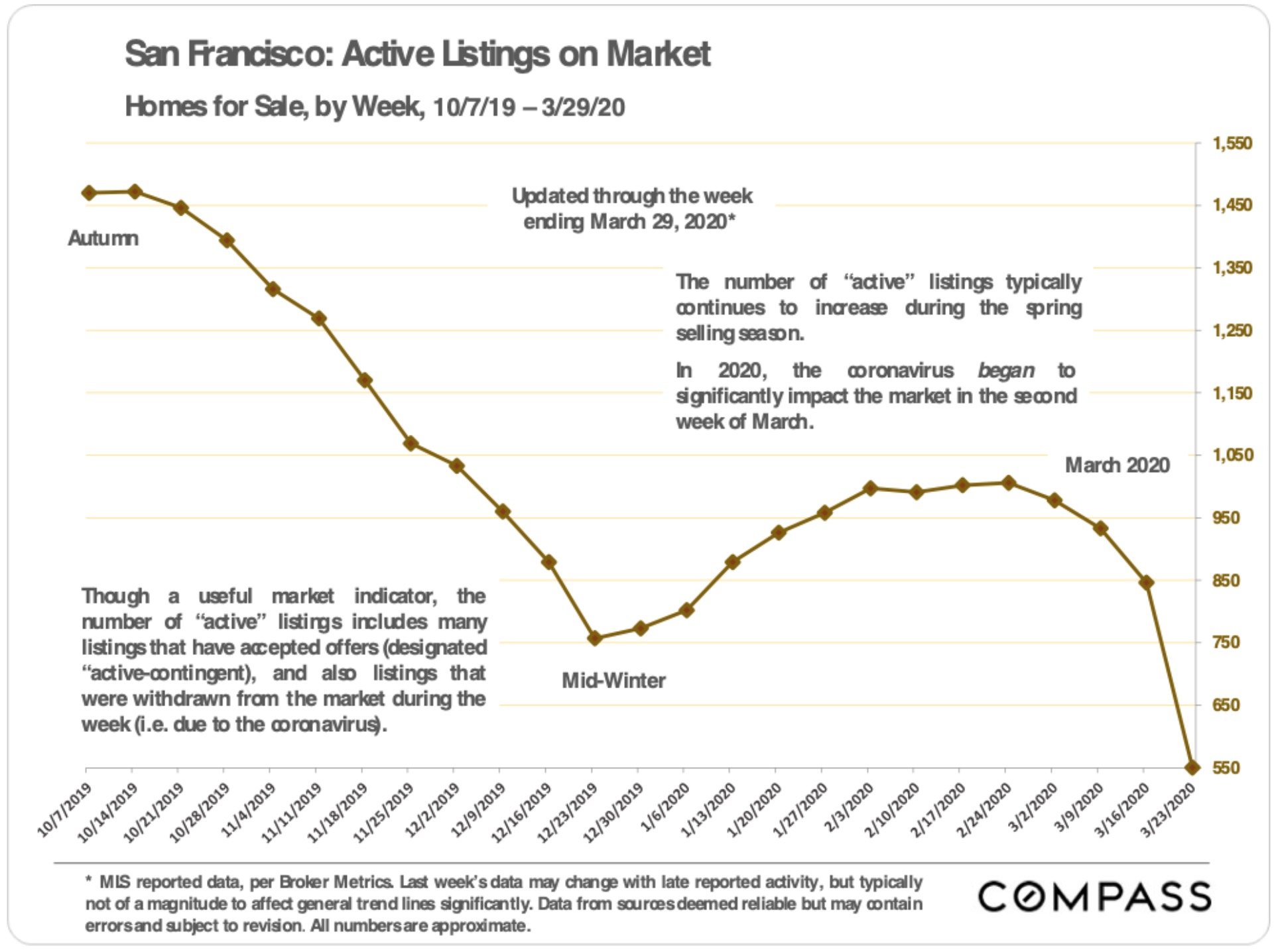

In any normal year, new listings surge starting around February and into the Spring. Instead, starting shortly after Mayor Breed’s and Governor Newsom’s “shelter in place” orders of March 16 and 19, new listings tumbled to levels normally seen in the heart of winter. In short, except for transactions in process, residential real estate came to a hard stop in San Francisco. No open houses, no private showings, no lender appraisals, no renovations, no staging. I know from personal experience: I currently have three listings that were scheduled to go “live” in late March. They are all on hold.

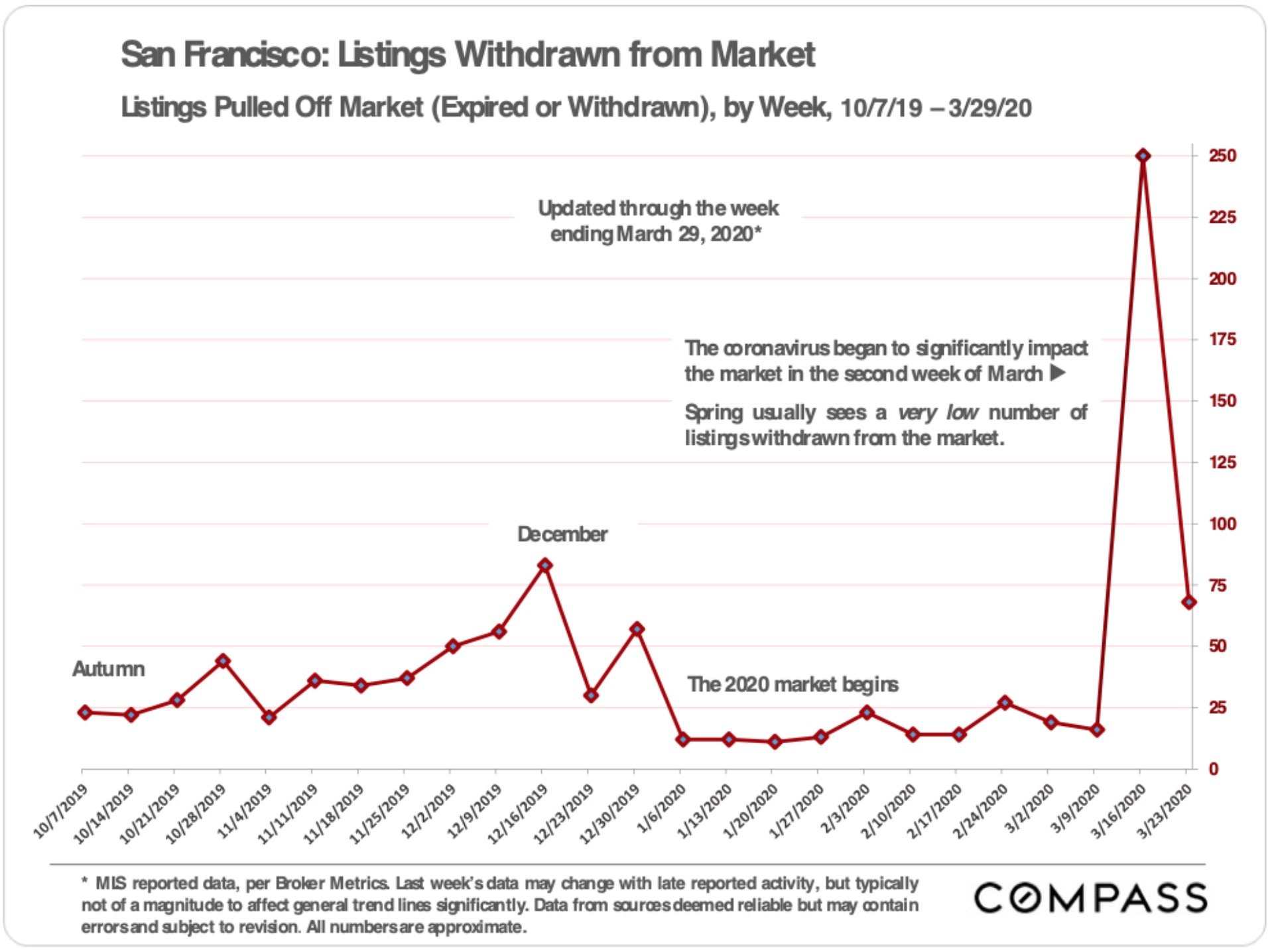

Meanwhile, properties that were on the market have been “withdrawn” in record numbers (see below). In addition, the San Francisco Association of Realtors (SFAR) has created a new status called “Hold,” in which properties can technically remain listed on the market without having their “days on market” count against them. This possibly explains the drop in the number of Withdrawn listings for the week of March 23, as properties were shifted to that category.

The combined effect of no new listings and a huge number of withdrawn listings has resulted in very few remaining “Active” listings being on the market – the opposite of the usual Spring cycle.

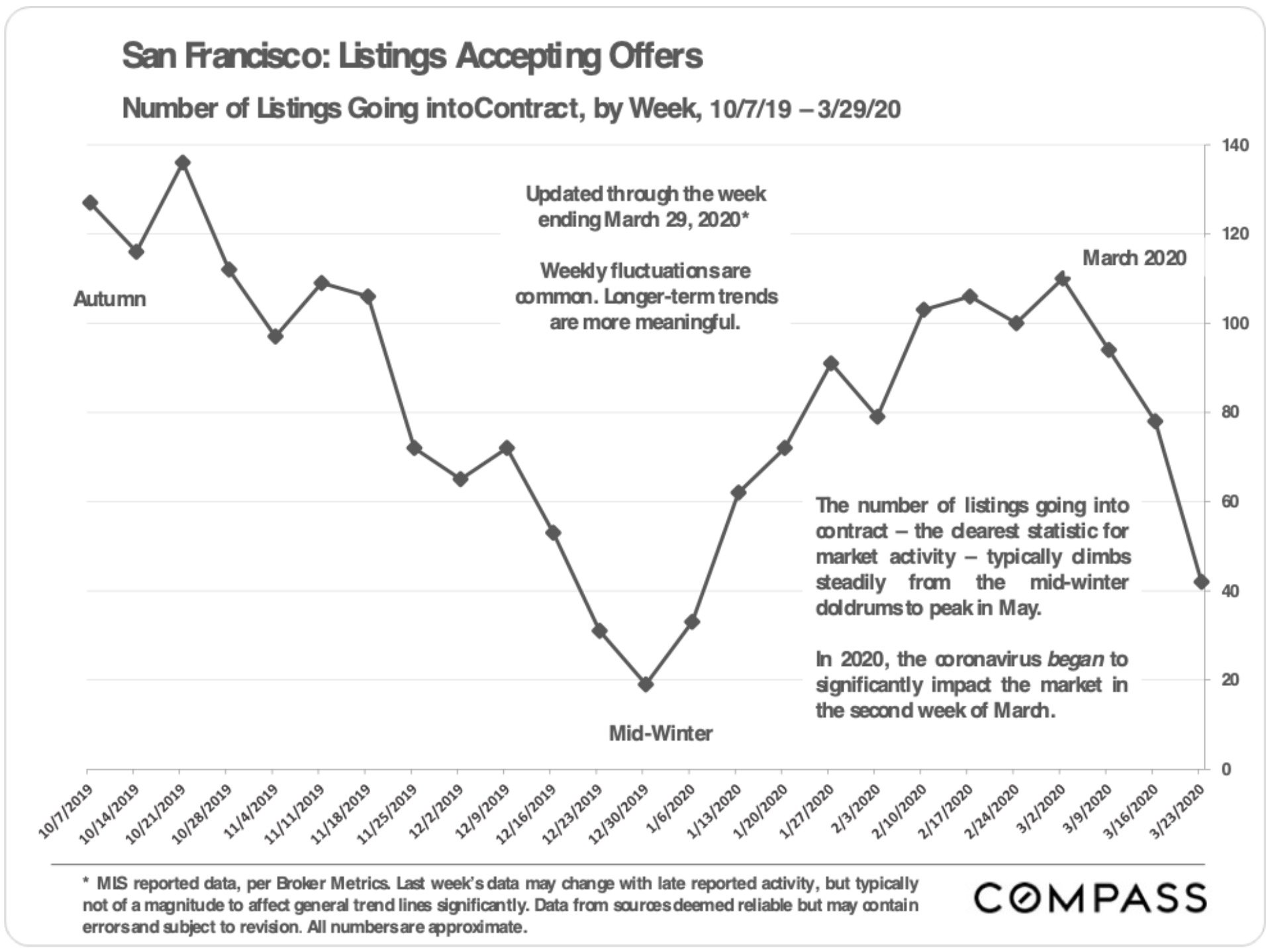

If the supply side has dropped off a cliff, demand is following suit, as the next chart shows. Furthermore, the accepted offers that are still being recorded probably represent transactions in which buyers had already toured the property prior to the “shelter in place” order going into effect. The numbers may decline further in coming weeks.

What will the future bring? Hopefully, an avoidance of the worst outcomes – unthinkable death tolls, lost businesses, lost jobs, lost friends and family.

For the real estate market, in my view, it’s too soon to tell. Zillow has a white paper that reviews studies of pandemics including, SARS (2003), the Spanish Flu (2018) and early results from Covid-19 in China. The conclusion seems to be that real estate market values held steady while activity dropped, and that both activity and values rebounded when the crisis passed. Whether that will be the case this time is anybody’s guess.

Here’s my guess: the longer the crisis continues, the more likely it is that it will do long-lasting damage to the economy and the real estate market itself. If the crisis is short and businesses can hire back employees and the self-employed can get back on their feet, then I can certainly imagine a robust bounce back to pre-Covid activity and prices. But as the crisis drags on, I worry that it may take time for lost jobs and lost equity to come back. Like the proverbial tanker, if the global economy really slows, it will be hard to get it going again. An article in today’s NY Times said as much.

Despite our current challenges, I absolutely believe that San Francisco is better-positioned than most places in the world to weather and ultimately recover from this pandemic, both physically and economically. All of the things that make this a great place to live and work remain in place.

Meanwhile, I am doing lots of walking (Luna is grateful!) and discovering hidden places I never knew about, despite many decades of living here. One recent discovery: Tank Hill and Pemberton Lane Stairs, just below Twin Peaks. You can read more about them here.

Stay safe, everyone. As always, your questions, comments and referrals are much appreciated!

Misha