A client of mine recently opined that he thought that Pacific Heights and other luxury neighborhoods were “overdue for a bump” in home prices. He thought that well-heeled Millennials and Gen-Z-ers were neglecting the north side of the city in favor of hipper locations like Mission/Valencia Street, Duboce Triangle, Hayes Valley and, of course, the perennial favorite Noe Valley.

As someone who has lived and worked in SF for over 30 years, I’ve witnessed my share of cycles where people bid up the “up and coming” neighborhoods (Bernal Heights is the poster child) as they get priced out of their “A-list” neighborhoods. However, when the market turns down, those same neighborhoods tend to get hit hard as buyers shift their attention back to their first choice. So, my hunch was that over the long-term, neighborhood appreciation rates would be about the same.

It turns out that I’m mostly right. The chart below shows both total appreciation and compound annual appreciation for various neighborhoods in the city within their MLS (Multiple Listing Service) Districts over the last 20 years.

While the Inner Mission and Bernal Heights have in fact appreciated more and faster than elsewhere, most city neighborhoods are right at around a 7.5% increase year over year. This fits with my general view that you could buy a single family home pretty much anywhere in the city and do alright over the long-term.

Why? First and foremost, SF is always going to be a popular place to live – notwithstanding its challenges. Secondly, single family homes are a shrinking part of the housing market. “Land,” as Will Rogers famously said, “they ain’t making any more of it.” The city’s stock of single family homes is constrained by geography – but demand continues to grow.

In fact, as I’ve described elsewhere, sales inventory is actually falling as more and more people choose to “age in place” for financial and lifestyle reasons.

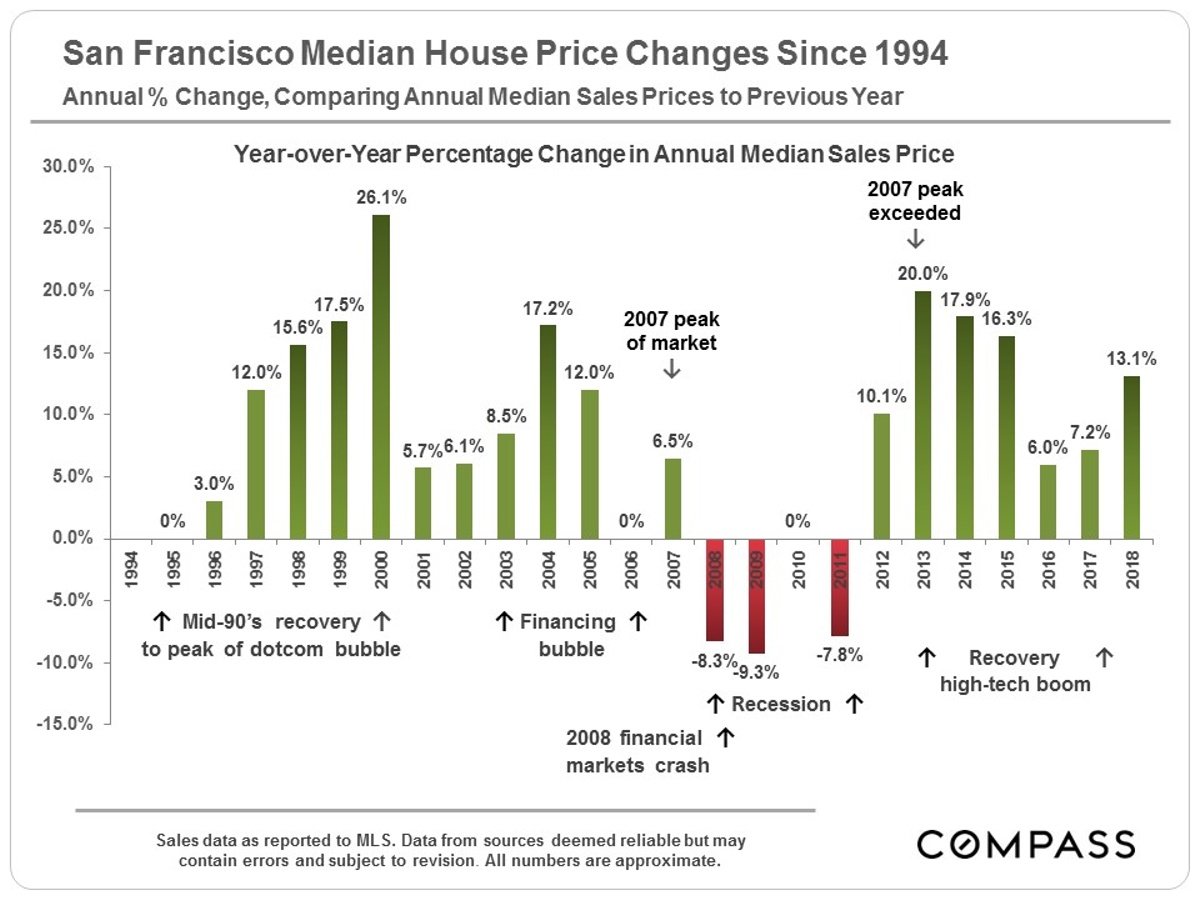

But back to our first chart and rates of appreciation. The big exception is the cluster of luxury neighborhoods in MLS District 7: Pacific and Presidio Heights, Cow Hollow, and the Marina. Here, the rate of appreciation is significantly lower than elsewhere. Why? Well, consider that the base starting price is significantly higher. Back in 1998, you needed $1.6 million to buy a house in those neighborhoods – three to five times what you needed for other neighborhoods. I’m no economist, but I suspect that these neighborhoods will always approach the upper limit of what people are prepared to pay for a home. There’s simply less headroom for them to move up in price.

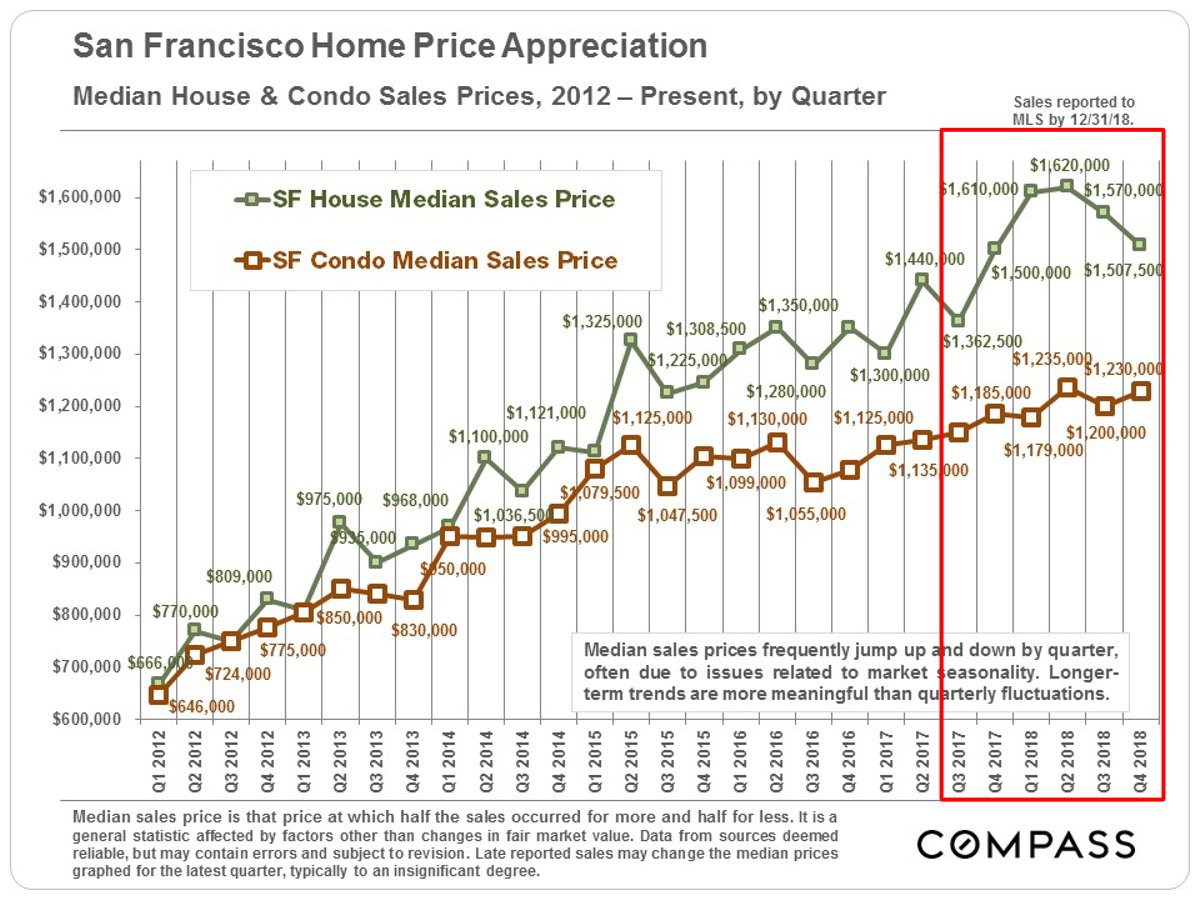

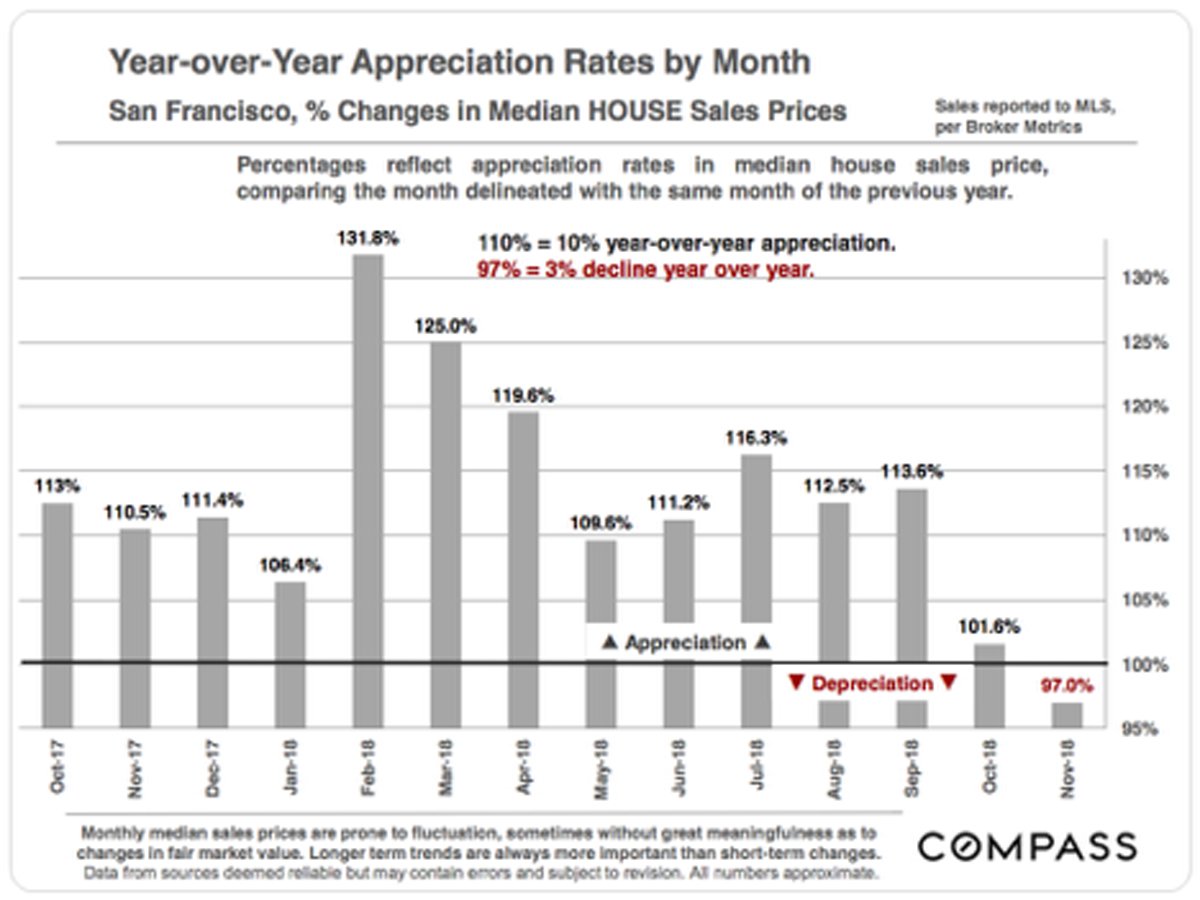

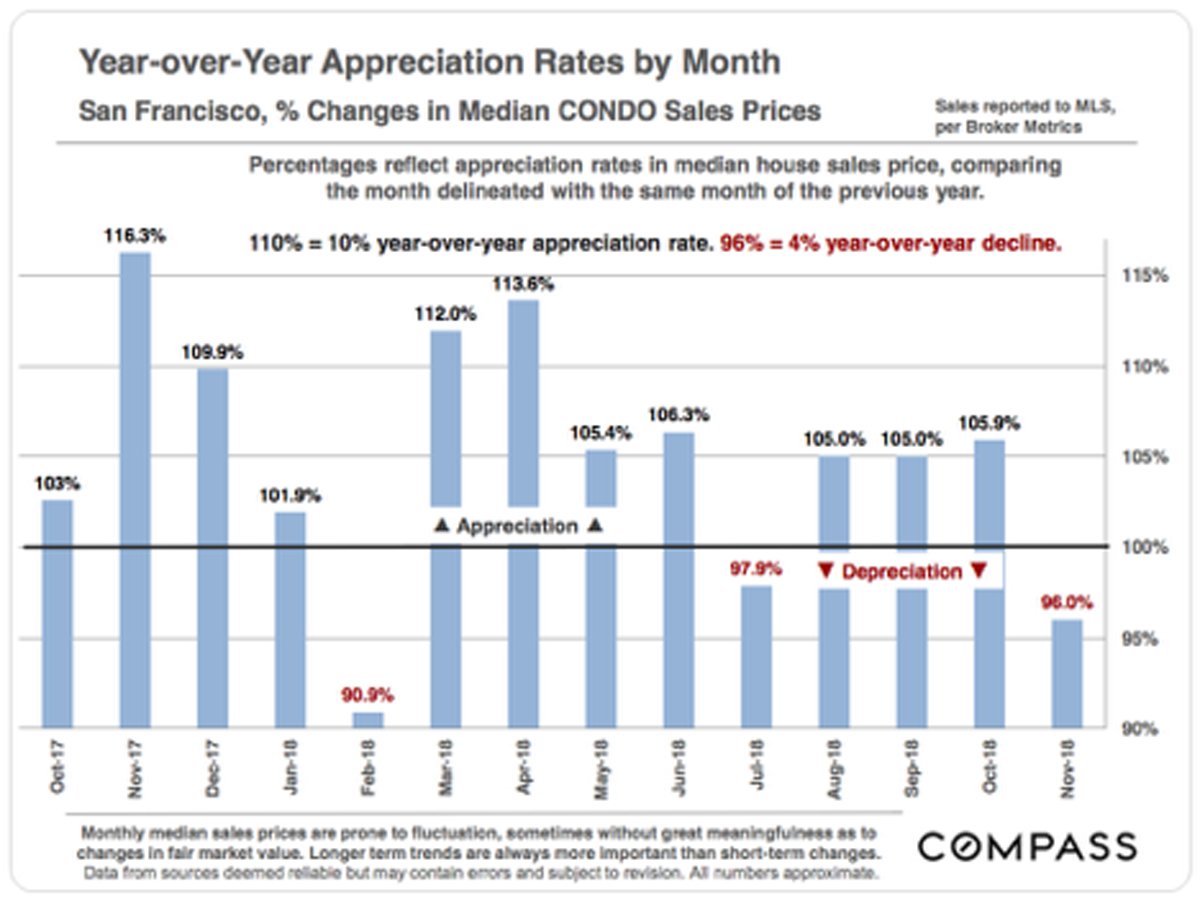

It’s also worth remembering that cumulative appreciation over a long period can obscure short-term fluctuations, as the following chart shows. That’s why I generally counsel my clients not to buy a home if they’re not planning on holding onto it for at least 5 to 7 years.

Here’s a comparative look at median home price trends in select neighborhoods, updated through 2018.

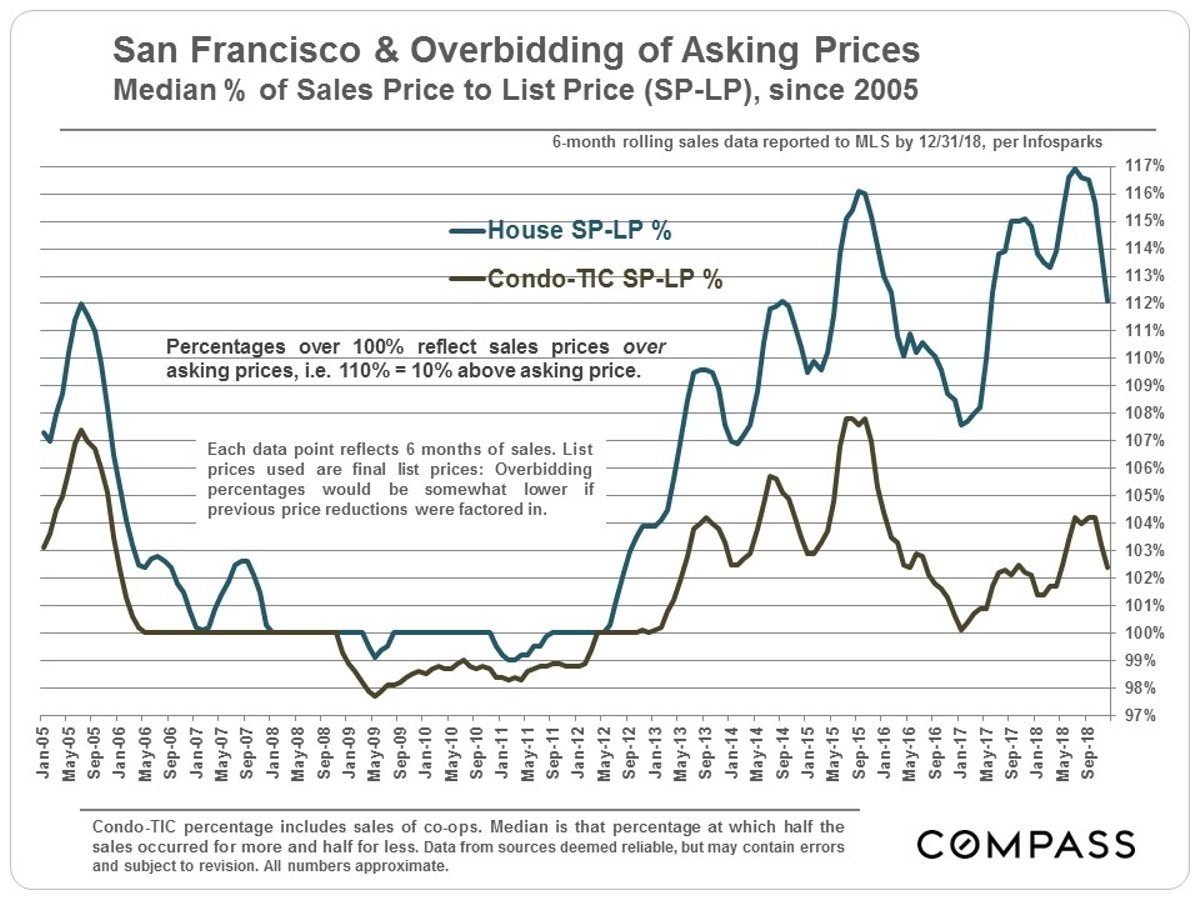

And while I believe that it is folly to base an offer on statistical averages for “list” to “sale” prices, the following chart does reflect which neighborhoods are seeing a lot of buyer interest. Here’s the takeaway: just as you’d expect in a mature “up” market, it’s the more affordable neighborhoods that are seeing the highest level of interest as buyers are priced out of the more expensive ones.

I have a comprehensive table of median home prices by neighborhood and bedroom count for every MLS District in the city, updated through May 2019, as well as a similar table for condos. Unfortunately, there’s no easy way for me to display it in my newsletter. If you’d like a PDF of the table or are curious about a specific neighborhood, please email me and I’ll be happy to send it to you.

As always, your questions, comments and referrals are much appreciated!

Misha