A couple of months ago (gasp!) I promised to post my favorite charts from the UC Berkeley Fisher School of Real Estate and Urban Economics’ symposium on the state of the market. I then got swamped working on my own development project up in Windsor, north of Santa Rosa, and all my blogging came to a halt. Without further ado, here are a few of my favorite charts from the conference. In most cases, I’ll let them speak for themselves.

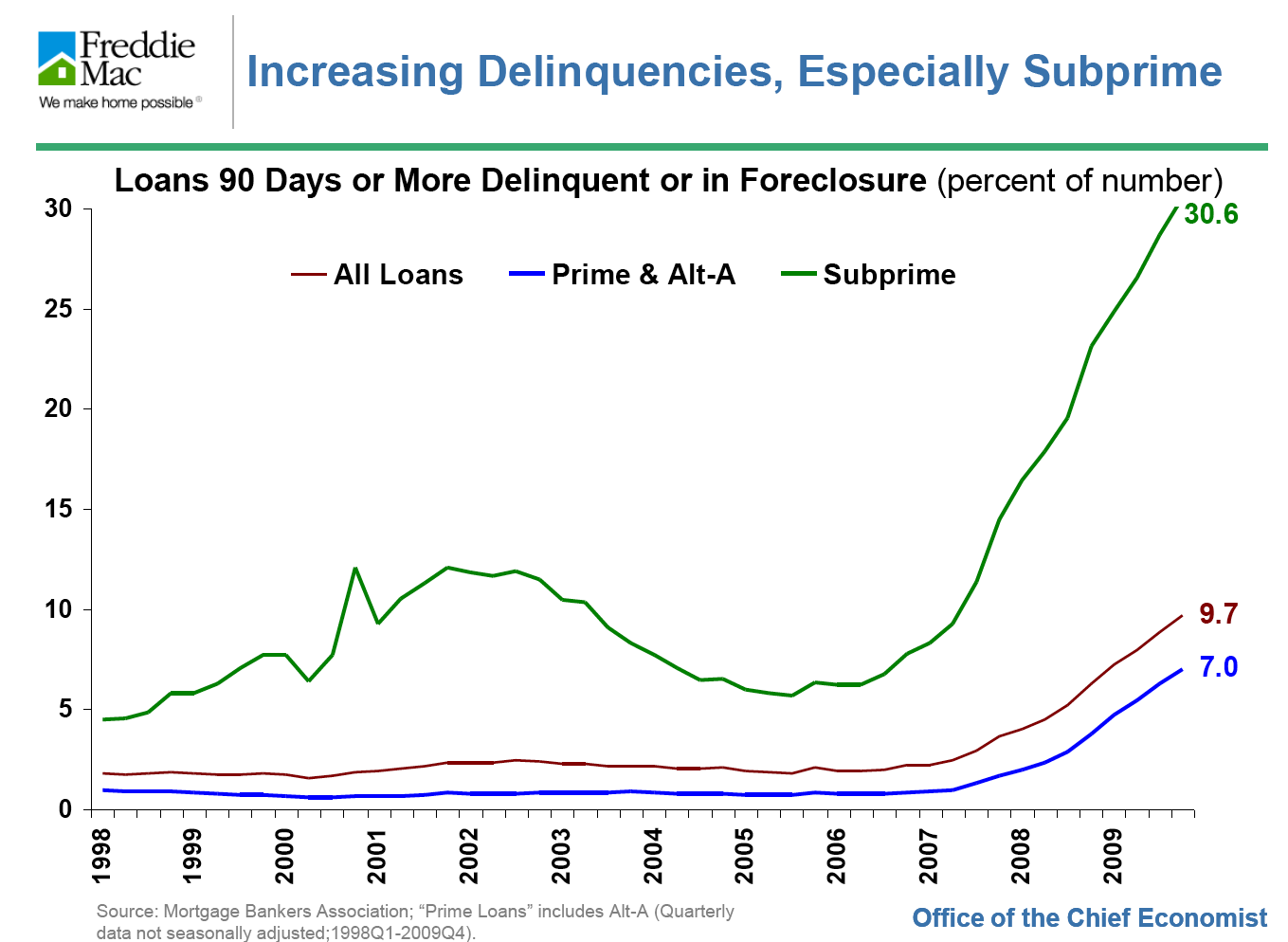

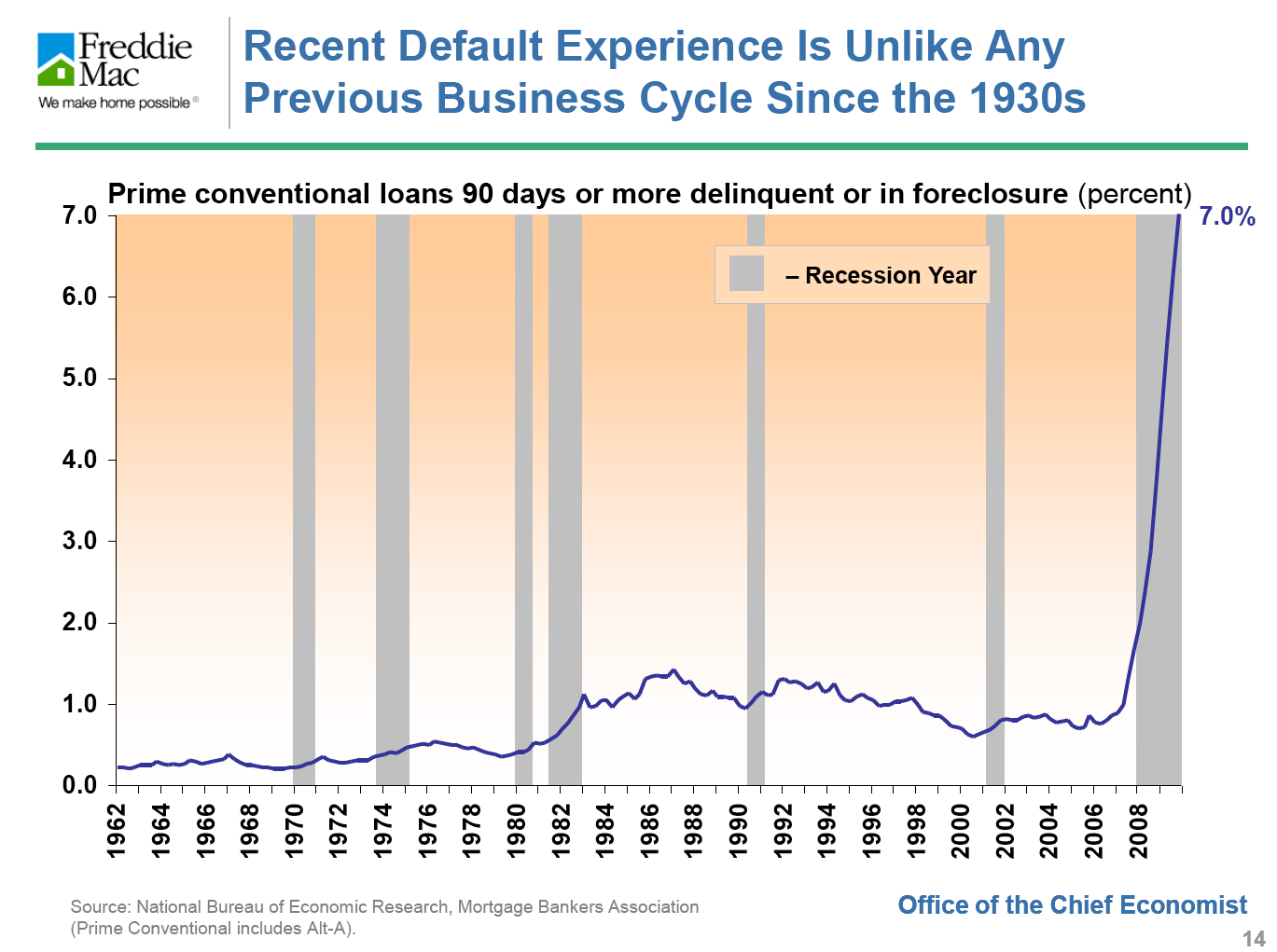

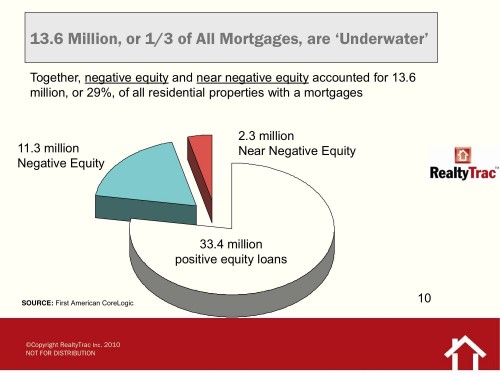

Delinquency RatesForeclosure ratesLoans at or near negative equity

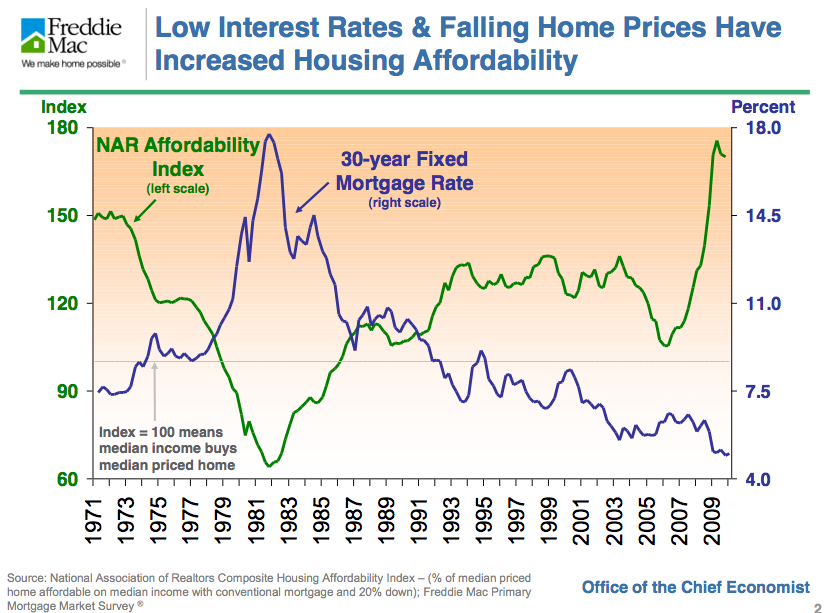

Among the scions of the real estate industry presenting at the Fisher Conference (see my previous post) was none other than Frank Nothaft, Chief Economist and Vice President of Freddie Mac. He had a doozy of a slide set. Here’s one my favorites. More to follow.

The chart shows that nominal (ie. not inflation-adjusted) prices hadn’t shown an actual decline in over 50 years prior to 2006/7. Real (inflation-adjusted) prices have fallen in previous recessions, though with the exception of 1980-82, those declines were pretty small. This time round, though, we’re down big-time.

An inflation-adjusted annual average price growth of 1.3% sure doesn’t sound like much to me. And that number’s not going up a lot even if you discount the suislide of the last three years. Proof that a home isn’t a “good investment?” I’ve never suggested that it is.

Doesn’t look a whole lot better even after you factor in leverage. If you’ve put 20% down, the rate of return on your equity increases five-fold. Now we’re up to a whole 6.5% gross return. But that’s before all the expenses of ownership not to mention the endless lists of things “to do.”

Of course, the real reason to buy a home is because it’s about “shelter” in the broadest sense of the word. It’s as basic as finding a comfortable cave for yourself and your loved ones and painting beautiful drawings on the walls.

Just back from the Fisher Center for Real Estate and Urban Economic’s semi-annual symposium on all things real estate. (FCREUE is the real estate department within UC Berkeley’s Haas Business School.)

Ken Rosen is the Center’s oft-quoted co-chair and quietly advises real estate investment funds with over $300 million in assets. Most of the time these symposiums take a very high-level view of real estate: it’s an asset class to be compared to other assets, and the focus is usually on institutional investors and broad real estate segments.

But with the housing melt-down, recent symposiums have been very much about the lowly residential market, both national and local, albeit within the wider context of the economy as a whole.

Rosen almost always delivers a fact and slide-packed economic forecast. It’s a big part of why I go. Here are some of his current observations and predictions:

The Shape of the Recovery:

Chances of a fragile recovery: 55%. We’ve already had a big bounce; he expects a slowdown for the rest of the year (This is a broken “W”)

Chances of a moderate recovery: 35% (This is the “U”)

Chances of a mild recession: 10%, (Think an “L” with a sinking bottom.)

Jobs: He thinks the job situation will turn around by the end of 2010 (other speakers weren’t so sure.) San Francisco has already started adding jobs.

Interest Rates: Rosen thinks that the Fed is already missing the boat on inflation and that it’s inevitable. Just as important, he thinks that the Fed should already be raising short-term interests, though he thinks it’ll keep them at near zero for another six months or so.

“Two years from now, short term interest rates will be back up to 4%.”

As for 30 year fixed mortgages, if rates go up to 6%, the real estate market will probably still be ok. If they go to 7%, we’re in trouble.

Home Prices. US Single family home sales will look good for the next few months but then will slow towards the end of the year. Lots of people are coming back on to the market because they see movement and because of the tax credits.

And now the takeaway:

“If you feel secure [in your job], now is a good time to buy because interest rates are going to go higher and prices probably won’t go much lower.”

Oh, and one last thing: Short China real estate. They’re in a massive bubble of their own.

Related articles by Zemanta

The View From Space: 2010 (pegasusventures.net)

No bubble in the real estate – Shaun Rein (chinaherald.net)

Back in the still-uncertain days of September 09, every market pundit had his or her own letter for what shape the recovery would take. I blogged about Ben Bernanke‘s “U,” Liz Ann Sonders‘ “V,” and Nouriel Roubini‘s “W” here. Though one could argue the jury is still out, I think it’s fair to say that Liz Ann won round one. The recovery is looking and feeling like a “V” — and in fact is falling pretty much within historical patterns. (Full disclosure — I had my money on Nouriel.)

I recently spent 20 minutes listening to her most recent webcast, and it all sounds pretty seensible. What I like about Sonders in particular is that she’s basically a contrarian. So many people are betting against the stock market’s phenomenal rise right now — and in favor of bonds — that she thinks that the bears are refusing to accept the fact that a solid recovery is in place. I like the way she puts it in a related article:

Skeptics are often the loudest folks in the room, and the bear case is often the more “intellectual” case, but the market has a tendency to reward the minority view, not the majority view.

What’s all this got to do with San Francisco residential real estate? One of her points touches on a theme that I’ve sounded here recently. As everyone knows, interest rates are likely to rise as the economy starts to strengthen and the Fed starts turning off the easy credit spigot. Sonders is not predicting the stratospheric rates that occurred in the early 1980’s. Nevertheless, it doesn’t take much of an increase in rates to have a significant impact 0n the amount of house you can buy.

Say you’re thinking about borrowing $700,000 on a 30 year fixed rate loan at the current rate of 5.25%. Your payment would be just under $3,900 a month. Now say that interest rates increase by just half a percent to 5.75%. Your monthly payment would increase to just under $4,100 a month. Maybe a difference of $200 a month doesn’t sound like that much: a couple of fancy restaurant dinners would would cost the same.

But look at it this way. Say that the the maximum you’ve decided — or the bank’s decided — you can afford to pay each month on your mortgage is $3,900 a month. Now that half percent increase in rates means that the maximum loan you can qualify for is around $662,000. That’s a loss of $38,000 in the amount you can borrow and the amount of house you can buy.

Last week, Case-Shiller released January data for its closely watched national housing index. Nationally, things are looking up – well, make that flat. And that’s good news. In the wonderfully backward language of the report, the index’s year over year rate of decline “improved.” Basically, we are back to where housing values were a year ago.

Since for most of us our homes represent our biggest asset, that’s pretty good news when you consider how bleak things looked back in March of 2009. Just think of how you were feeling about your 401(k)s.

But before you break out the champagne, consider that national home prices have now “recovered” to levels last seen in Autumn 2003. That’s over six years of appreciation wiped out.

The San Francisco Metropolitan Statistical Area (that’s 5 of the 9 Bay Area Counties, folks) is up 15.2% from its trough value. Case-Shiller does not break out San Francisco proper from the much larger MSA. However, I calculate that median prices in January were up just 10% from the lows reached in March 2009. (I use 3 month moving averages, which approximates the seasonal adjustments the CS Index uses.) To see how SF did through 2009, check out my blog and charts here.

In an article entitled Great Time to Buy (Famous Last Words), last Sunday’s New York Times took a swipe at perennially optimistic real estate agents who have never seen a time that wasn’t a good time to buy a house. Fair enough. Self-interest and magical thinking are not limited to the real estate profession.

For the record, I’ve never suggested to anyone that buying a home is a good “investment.” You can do much better in the stock market and probably even in bonds.

However, I am beginning to think that if you’re going to shackle yourself to a home, now may not be a bad time to buy. And I think the NY Times article supports my position.

Why do I think so? Most of the articles I’ve been reading suggest that the worst is over in terms of price declines, this article included. That doesn’t mean that prices couldn’t drop another 5 to 10%. But it’s a fool’s errand to try to predict the bottom (or top) of any market.

At the same time, the consensus seems to be that interest rates have nowhere to go but up, given the huge stimulus that the government’s been giving to prop up the economy. One can argue whether and when the government should choke off the spigot of easy credit, but when it does, rates are going to have to go up.

Here’s the takeaway from the NY Times article:

“Instead of betting on home prices, you make a bet on whether money will become cheaper or more expensive, allowing you to buy more or less house.”

Now it’s true that increasing interest rates ultimately lead to declining prices as tighter credit drives down demand. That’s the theory anyway. But after the huge declines we’ve already seen, it’s anybody’s guess as to when, where, or how that will happen. As the article says, “don’t go there. Maintain your focus.”

Here’s a graph from mortgage-X.com on historical blended (ie. fixed, arms, etc.) mortgage rates. Should make people who can qualify for a mortgage in this still-crazy market feel pretty good, no?

Ken Rosen is a smart guy. He’s the co-chair of the Fisher Center of Real Estate and Urban Economics at the Haas School of Business at UC Berkeley and the investment adviser of choice to some of the biggest players in real estate, from banks to insurance companies to REITS. Ken might not be able to appraise your house, but he could tell you how each sector of the real estate economy has fared anywhere in the country, and probably in many parts of the world.

Once or twice a year I spend the day in a windowless hotel conference room listening to Ken and some of the biggest heads in the real estate biz expounding on the state of real estate. These guys (and they are mostly guys) look at real estate through the lens of global macro-economics and finances. Want to know where interest rates are going? They study yield curves on T-Bills and monetary policy in the capitals of Europe. This is “the view from space.”

I reported on Ken’s predictions from November of 2008 here. (Remember, we were already in deep doo-doo, though things got worse through the first quarter of 2009.) Before moving into his predictions for 2010 and beyond, I thought it would be useful to see how well he did on on his forecasts for 2009:

The Ken Rosen Scorecard for 2009

Chance of a deep recession: 70%. Bingo.

S&P 500 at year-end under a deep recession: 850. Actual: 1115. Woops (but who said the market was rational?)

The dollar:“Will continue to do well.” Nope, it lost ground.

Not a great batting average you say? Truth is, I’m cherry-picking here. Overall, Rosen’s message in November 08 was that things were improving, but that there would be volatiility and a long, slow recovery in housing. Notwithstanding our brush with death in March — Rosen put the chance of a deep recession at 5% — his prediction on that aspect of the market seems to be holding up well. As for the dollar, given the gaping chasm that faced the global markets in the early months of 2009 – led by crashing and burning US financial institutions – the dollar’s decline shouldn’t be a surprise.

And as for the stock market and its amazing recovery, given what still seems to be looming on the horizon, I just can’t figure that one out at all.

Rosen’s Predictions for 2010

In terms of the shape of the recovery, Rosen estimates the chances of a “broken W” — read fragile recovery – at 65%. This is where I’m putting my money folks.

He estimates the chances of a more robust recovery at 25%, and that of a long , Japanese-style recession at 10%.

Expect a slow, fragile recovery, a bottoming out of the housing market, and rising long-term rates.

Estimates for the Stock Market, Year End 2010

S&P 1150; Dow 11,000

Advice for the Home-Buyer:

If there’s any good news here, it’s that Rosen thinks that the sector will come back fastest is single family housing.

Here’s the takeaway quote:

“Take advantage of the windfall tax credit and low interest rates if you’ve got a good job”

Rosen thinks that prices have bottomed (I’m not so sure). But it does appear that

REO’s (properties taken back by the banks) have declined as a percentage of all sales, and that should help to stabilize prices.

From a socio-economic perspective, housing affordability has increased significantly due to low interest rates and price declines, and that can only be viewed as good if you believe that widespread home-ownership is a public “good.” (I do.)

What could go wrong?

In a moment of brilliant serendipity, Rosen’s co-chair at the Fisher School, Bob Edelstein — no small brain himself — happened to sit next to me at lunch. In the next 30 minutes we covered everything from wine to Waziristan. His outlook was not as sanguine as Rosen’s. We didn’t get into details, but my impression was that Edelstein was more concerned than Rosen about a jobless recovery coupled with higher interest rates driven by enormous deficits.

Once again, the magic eight ball says: “Ask again later.”

George may have left office a year ago, but there appears to be a growing consensus that the likely shape of the recovery will be a “W.” How appropriate, if you believe that we are reaping the bitter fruit of his administration’s policies.

A front page article in the Business Section of last Wednesday’s New York Times, grimly entitled “An Upturn in Housing May be Reversing,” pulls together recent and contradictory data from various sources, including Case-Shiller, Moody’s, and The National Association of Realtors. The conclusions are sobering.

There is a growing consensus that the positive national sales data that we’ve seen over the last few months is faltering. Much of the recent activity, for example, was stimulated by the anticipated expiration of the “First Time Home-buyer Tax Credit,” originally set to expire in November, and now extended through April of next year. Essentially, this means we’ve “borrowed” from future sales.

Also, despite some positive economic news and decent sales volumes, there’s been little improvement in sales prices because inventory levels – read “foreclosed properties” – remain so high. Mary Maitland, VP of the S & P Index that publishes the Case-Shiller Index foresees a “W” pattern for the housing market, with prices this winter testing the lows we saw earlier in the spring. Am I allowed to say “I told you so?”

The NY Times article has a cool interactive chart for specific MSA areas including “San Francisco” — remember this covers 5 of the 9 Bay Area Counties.